Commercial Credit Circuit (C3)

A Financial Innovation to Structurally Address Unemployment

by Bernard Lietaer

in collaboration with STRO (www.strohalm.nl)

What started as a banking and financial crisis in 2008, is now rapidly becoming a major job crisis. It is also a well-known fact that the vast majority of jobs are provided by small and medium sized enterprises (SMEs). And the survival of many such firms is now at risk because of cash flow problems.

The Problem

SMEs’ are being pressured by suppliers for prompt payments, say within 30 days; while their larger customers pay them only in 90 or more days. This becomes a deadly cash flow trap whenever banks refuse to provide bridge financing, or do so at steep conditions. This problem has become more critical recently in developed countries under the impact of the financial crisis, but it has long been an endemic issue in developing countries.

The Solution

The “Social Trade Organisation” (STRO), a Dutch Research and Development NGO, has successfully developed business-models over the past decade in several Latin American countries which culminated with a financial innovation that structurally addresses this precise challenge. The process uses insured invoices or other payment claims as liquid payment instruments within a business to business clearing-network. Each recipient of such an instrument has the choice to either cash it in national money (at a cost), or directly pay its own suppliers with the proceeds of the insured invoice. How this is achieved is described next.

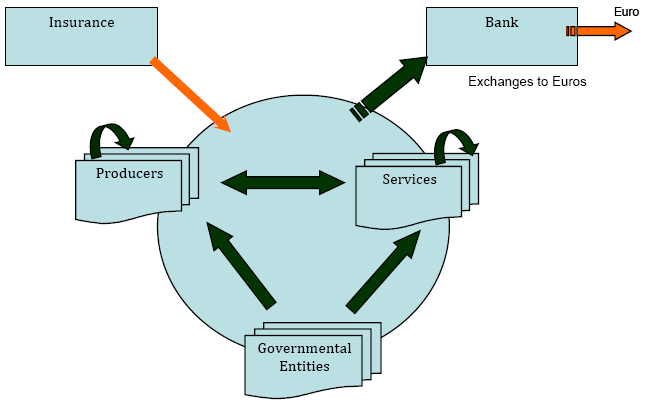

C3 Step by Step

The C3 mechanism involves the following six steps:

- Participating businesses start by securing an invoice insurance up to a predetermined amount, based on the specific creditworthiness of their own business and of the claims they obtain on third parties.

- The business that has obtained such an insurance (hereafter referred to as business A) opens a checking account in the clearing-network, electronically exchanges the insured invoice for clearing funds, and pays its supplier (business B) immediately and fully with those clearing funds via the clearing network.

- To receive its payment, business B only needs to open its own checking account in the network. Business B has now two options: either cashing it in for conventional national money (at the cost of paying the interest for the outstanding period, e.g. 90 days; plus banking fees); or pay its own suppliers with the corresponding clearing funds (at no cost).

- Whatever the timing of the payment is to business A, business B is in a position to use the positive balance on its account in the network, for instance to pay its supplier business C.

- Business C only needs to open an account in the network. It has then the same two options as business B: cash it in for national money, or spend it in the network. And so on…

- At maturity of the invoice, the network gets paid the amount of the invoice in national money, either by business A or by the insurance company (in case of default of business A). Whoever owns at that point the proceeds of the insured invoice can cash them in for national money without incurring any interest costs.

Benefits

For businesses:

- Businesses increase their access to short-term credit as needed to improve their working capital and the use of their productive capacity. The size of this credit can be built up to a stable level between a quarter (covering therefore up to an average of 90 days of invoices) and half of annual sales; at a cost substantially lower than what is otherwise possible.

- Suppliers are paid immediately, regardless of the payment schedule of the original buyer, injecting substantial liquidity at very low cost in the entire SMEs network. The approach provides a viral spreading of participation to the C3 networks from clients to suppliers.

- The technology is a proven one, doesn’t require any new legislation or government approvals, and the necessary software is available in open source.1 Only invoices and other claims that are 100% guaranteed, and 100% computerized, are acceptable in a C3 system. C3 thereby encourages the generalization and more efficient use of IT infrastructure among SMEs, including the opening of new markets and marketing channels through e-commerce.

For governments, particularly regional governments:

- The C3 approach is a dependable way to systemically reduce unemployment. Governments at different levels (EU, national, regional) can contribute to a joint guarantee mechanism. Such a guarantee mechanism is considerably cheaper to fund than subsidies or other traditional approaches to reduce unemployment.

- C3 systems are best organized at a regional level, so that each network remains at a manageable scale. Businesses with an account in the same regional network have an incentive to spend their balances with each other, and thus further stimulate the regional economy. C3 provides a win-win environment for all participants, and therefore promotes other collaborative activities among regional businesses.

- Each C3 network should use the same insurance standards and a compatible software so that they can interconnect as a network of networks to facilitate exchanges internationally For banks and the financial system:

- The win-win approach of C3 includes also the financial system. As the entire C3 process is computerized, it significantly streamlines the lending and management for the insurance and loan providers. SMEs can therefore become a more profitable sector for banks, because the credit lines are negotiated with the entire clearing network, providing the financial sector with automatic risk diversification among the participants in the network. In the upcoming surge of new competitors in the market – such as Facebook, Google or Tesco currencies and banks – this monetary innovation provides an additional window for banks to sell their core activities.

- Most banks are also involved in providing insurance services. C3 opens for them a whole new market for insurances and credit, all the way down to services for microfinance enterprises. As C3 is completely computerized, even such individually small-scale entities can now be serviced at a very low cost.

- The C3 mechanism systemically contributes to the stability of employment and of the entire economy, which is helpful for the overall solidity of the banks’ portfolios.

1 Open Source means that the source code of the software is publicly available, making it possible for users to adapt the system to their own requirements. Specific parts of the C3 methodology are protected by a patent, but the conditions to get user licence are transparency and monitoring procedures to guarantee fair treatment of the network participants, as well as a small contribution to fund the spreading of such systems. This generates the benefit of additional spending opportunities for existing network. More information via c3@socialtrade.org .